How to Get a Second VA Loan Use Your VA Entitlement

Table of Content

Twelve months is considered the longest allowable delay, no matter what. But if a veteran plans to retire within 12 months, that can also justify an extension. Similarly, a veteran who plans to retire to a vacation destination can get around the workplace proximity rule. Get a Quote A VA approved lender; Not endorsed or sponsored by the Dept. of Veterans Affairs or any government agency. The VA’s second-tier entitlement allows you to take out another VA loan to buy a second home. It is very important for the buyer to consult with a recognized VA loan advisor before going for the loan.

It’s worth noting that things work a little differently if you only have partial entitlement left. This situation occurs when you get a new VA loan without paying off your old one. When you sell your home and pay off the loan balance, your entitlement typically automatically restores. However, your entitlement can be restored as many times as you sell a home and pay the loan balance in full. Let's say you buy a $200,000 home, and the VA guarantees 25% of the loan amount, or $50,000. Even with that $50,000 tied up in the first mortgage, you have $77,600 in remaining entitlement.

How long do you have to wait between VA loans?

This is offered to those who have paid off their VA loan in full but have not sold the property. Some borrowers avoid this option because they may be required to make a down payment in such cases. Others don’t mind the down payment as it can reduce the amount of the VA loan funding fee depending on the percentage of down payment made. If you have used your VA home loan benefits before, you have used some or all of your VA loan entitlement.

The offers that appear on this site are from companies that compensate us. This compensation may impact how and where products appear on this site, including, for example, the order in which they may appear within the listing categories. But this compensation does not influence the information we publish, or the reviews that you see on this site.

VA Streamline Refinance (VA IRRRL): What Is It And How Does It Work?

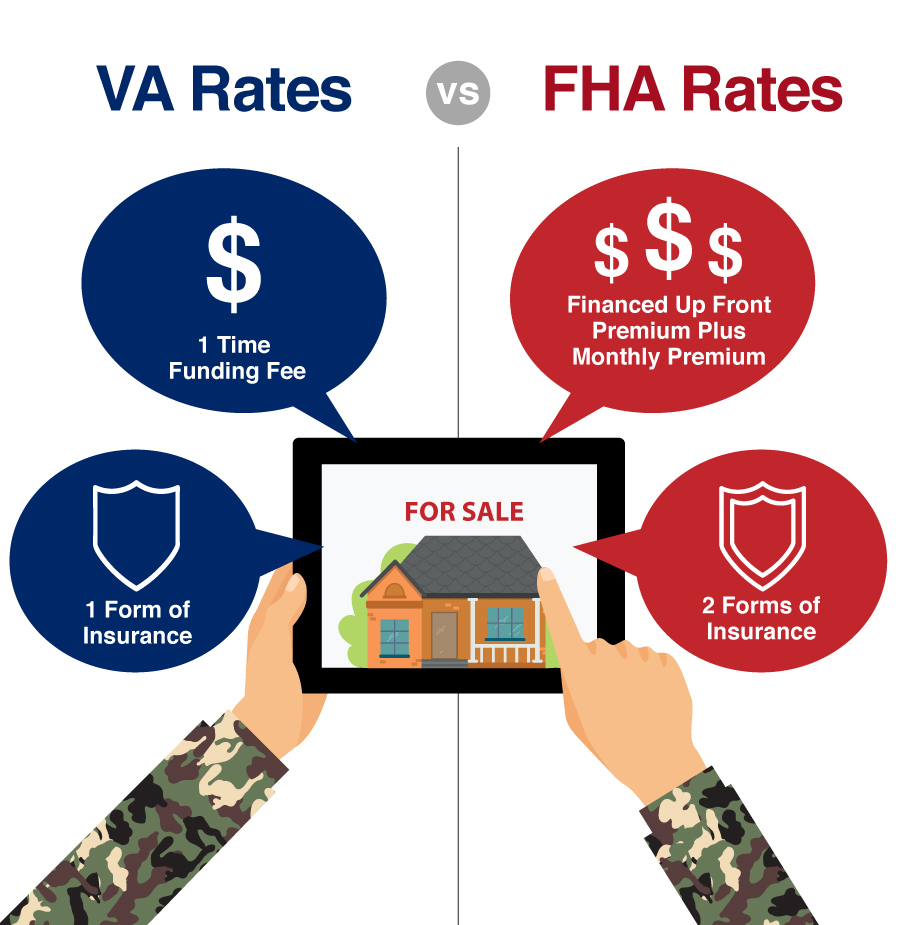

What we know now as the VA home loan actually began with the 1944 Servicemen’s Readjustment Act. Among other benefits (e.g. education and job training), this bill established the predecessor to the current VA home loan, increasing veteran homeownership via access to affordable mortgages. Because the VA funding fee is a percentage of your total loan amount, it could create a high financial hurdle for some home buyers.

It is important to note you need to restore your entitlement before you can apply for another VA loan. There are many myths and rumors surrounding VA loans, some of which deal with your eligibility for the program after you’ve already had a VA loan. If the buyer doesn’t agree, the entitlement you used to buy the home will remain tied up in the property until the new owner fully repays the loan. You have two or more VA loans for different homes at the same time. We’re transparent about how we are able to bring quality content, competitive rates, and useful tools to you by explaining how we make money.

Oct Can I Use A VA Loan For A Second Home, Rental, Vacation Condo, or A Manufactured Home?

This means you cannot legally purchase a home with a VA loan that you don’t intend to occupy for the majority of the year. Then you can either restore your entitlement or use your remaining entitlement to cover a new VA loan. In some cases, you can restore entitlement to obtain a cash-out refinance for the property you currently own.

To be sure a VA loan can be used in a particular circumstance, it’s a good idea to check with the regional VA office and discuss the situation. Buyers who have some of their basic entitlement remaining may be able to utilize that and avoid the minimum loan amount. You can ask a loan officer to go over your Certificate of Eligibility with you in more detail. For example, let’s say the limit where you want to buy again is $1,089,300.

In order to get a VA loan, you do not have to be a first-time home buyer, so using a non-VA loan in the past should not be a problem. In theory, if you meet the VA and lender requirements, you should be able to use a VA loan to buy a home in your new community. It is easiest to discuss what will happen if the property that was first secured by the VA loan has been paid off, and you wish to keep it. If you qualify, you may be able to receive a one-time restoration of your full VA entitlement if you qualify. The VA offers two refinance options, available exclusively to VA borrowers.

The basic entitlement amount is usually either $36,000 or 25 percent of the loan amount up to the conforming loan limit. Currently, $647,200 is the limit in most areas of the country, but it’s higher in some markets, up to $970,800. Then, you have a bonus entitlement, which is 25 percent of the $647,200 cap.

Rocket Mortgage will do VA jumbo loans up to $1.5 million without a down payment if you have a median FICO® Score of at least 640. You can get a VA jumbo loan as high as $2 million with a 680 credit scoe and 10% down payment or equity amount. As an example, let’s say Joan wants to buy a $300,000 house in an area with $647,200 conforming loan limits. She’s used $100,000 worth of VA entitlement in the past that hasn’t been restored. Borrowers with remaining entitlement are subject to the 2021 VA loan limit, which is $548,250 for one-unit properties in most parts of the United States. You can look up the exact conforming loan limit in your county on the Federal Housing Finance Agency website.

The VA cash-out refinance allows qualifying military borrowers to convert their home equity into cash. Sometimes borrowers can access as much as 100% of the equity in their current home. Technically, you can take out as many VA loans as you would like during your lifetime. Based on your remaining entitlement, you may not be able to tap into another VA loan until you sell the initial property you acquired through a VA loan. When pursuing a second VA home loan, you’ll need to have enough entitlement leftover from your first-time use.

Consequently, as you’re not actually selling the original house in this scenario, options for restoring your entitlement narrow. With assumable mortgages, a qualified buyer can take over, or assume, the original borrower’s mortgage. For VA borrowers, this means that, rather than sell your home, you can find a fellow veteran with VA loan eligibility to take over your mortgage payments and interest in the property .

Comments

Post a Comment